Financial Services

-

Home Buyer Mortgage

First Time Buyer Guide to buying your own home.

-

Home Mover Mortgage

Elevate your move with our tailored Home Mover Mortgage for a smooth transition to your new dream home.

-

Home Owner Remortgage

Refinance with our Home Owner Remortgage for better rates, releasing equity, or funding improvements—empowering your homeownership journey.

-

Buy-to-Let Mortgage

Dive into property investment with our Buy-to-Let Mortgage, tailored for both seasoned investors and first-timers seeking to build a profitable portfolio.

-

Holiday Let Mortgage

Transform your vacation home investment dreams into reality with a Holiday Let Mortgage,

-

Green Mortgages

Green Mortgages 🌳 are a new type of mortgage that rewards you for making your home more energy efficient.

-

Bad Credit

Mortgages Adverse Credit Mortgages 📉 are for people with a poor credit history.

-

Private Medical Insurance

Cut NHS wait times with private medical care and private hospitals.

-

Life Insurance

Pay off your mortgage if you or your partner die.

-

Bridging Finance

Navigate property transitions seamlessly with our Bridging Finance, offering quick and secure solutions for your short-term financial needs.

-

Auction Finance

Secure your auction triumph with Auction Finance, providing the financial backing needed to confidently bid and acquire your desired property.

Compare buy to let purchase mortgages with nationwide specialist mortgage advisers online. You can save money when you compare buy to let purchase mortgage rates with quotes from some of the leading mortgage providers in the UK.

The rules around landlord finance can be complicated from unusual properties, rental stress tests, limited company buy to let and more so for portfolio landlords. Your circumstances can limit options from minimum income, credit score and experience.

Lowest Limited Company SPV Buy-to-Let (BTL) Mortgage Rates

|

Rate

|

Fees

|

|

|---|---|---|

|

2.20%

2 Years Fixed

2

Years

Fixed

at

2.20%

|

|

|

|

2.25%

2 Years Fixed

2

Years

Fixed

at

2.25%

|

|

|

|

2.30%

2 Years Fixed

2

Years

Fixed

at

2.30%

|

|

|

|

2.35%

2 Years Fixed

2

Years

Fixed

at

2.35%

|

|

|

|

2.35%

2 Years Fixed

2

Years

Fixed

at

2.35%

|

|

The mortgage products shown are for illustrative purposes only and were generated 0 seconds ago. Always consult an independent financial advisor before proceeding with any mortgage. The figures are based on a £142858 property value, a £100000 loan amount and £42858 deposit. Initial Fixed Rate on a interestOnly loan, and a 25-year mortgage term.

|

Rate

|

Fees

|

|

|---|---|---|

|

2.20%

2 Years Fixed

2

Years

Fixed

at

2.20%

|

|

|

|

2.25%

2 Years Fixed

2

Years

Fixed

at

2.25%

|

|

|

|

2.30%

2 Years Fixed

2

Years

Fixed

at

2.30%

|

|

|

|

2.35%

2 Years Fixed

2

Years

Fixed

at

2.35%

|

|

|

|

2.35%

2 Years Fixed

2

Years

Fixed

at

2.35%

|

|

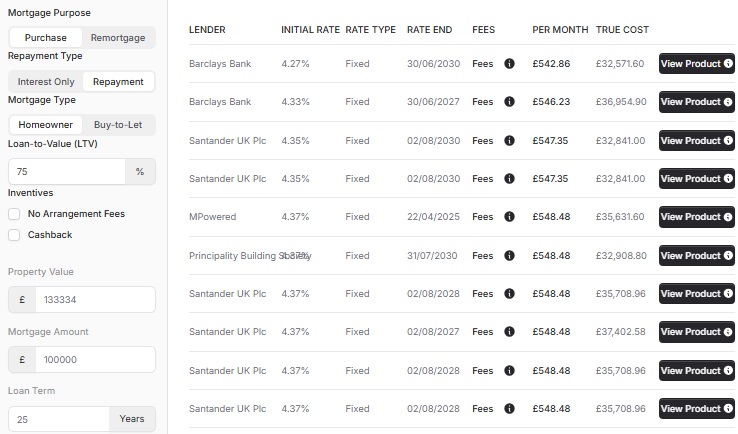

The mortgage products shown are for illustrative purposes only and were generated 0 seconds ago. Always consult an independent financial advisor before proceeding with any mortgage. The figures are based on a £133334 property value, a £100000 loan amount and £33334 deposit. Initial Fixed Rate on a interestOnly loan, and a 25-year mortgage term.

|

Rate

|

Fees

|

|

|---|---|---|

|

2.54%

2 Years Fixed

2

Years

Fixed

at

2.54%

|

|

|

|

2.80%

2 Years Fixed

2

Years

Fixed

at

2.80%

|

|

|

|

3.35%

2 Years Fixed

2

Years

Fixed

at

3.35%

|

|

|

|

3.35%

2 Years Fixed

2

Years

Fixed

at

3.35%

|

|

|

|

3.44%

2 Years Fixed

2

Years

Fixed

at

3.44%

|

|

The mortgage products shown are for illustrative purposes only and were generated 0 seconds ago. Always consult an independent financial advisor before proceeding with any mortgage. The figures are based on a £125000 property value, a £100000 loan amount and £25000 deposit. Initial Fixed Rate on a interestOnly loan, and a 25-year mortgage term.

|

Rate

|

Fees

|

|

|---|---|---|

|

5.26%

3 Year Fixed

TBC

TBC

Fixed

at

5.26%

|

|

|

|

5.92%

3 Year Fixed

TBC

TBC

Fixed

at

5.92%

|

|

|

|

5.94%

6 Year Fixed

TBC

TBC

Fixed

at

5.94%

|

|

|

|

6.29%

6 Year Fixed

TBC

TBC

Fixed

at

6.29%

|

|

|

|

6.49%

5 Years Fixed

5

Years

Fixed

at

6.49%

|

|

The mortgage products shown are for illustrative purposes only and were generated 0 seconds ago. Always consult an independent financial advisor before proceeding with any mortgage. The figures are based on a £117648 property value, a £100000 loan amount and £17648 deposit. Initial Fixed Rate on a interestOnly loan, and a 25-year mortgage term.

What is a Limited Company buy-to-let mortgage?

When buying a property to rent out in a limited company, you will often need a Limited Company buy-to-let mortgage.

A minority of Mortgage Lenders offer Limited Company buy to let mortgages. These mortgage products may differ from standard buy-to-let mortgages.

We can help you register a Limited Company (also known as an SPV), or your accountant. It is essential to register the correct SIC Codes and have a bank account in the company open for the mortgage direct debit.

As with a standard mortgage, they will base the lending on your personal circumstances. So a new SPV Company with no assets or income, set up on the same day, for example, is excellent. They will require personal guarantees from the directors/shareholders.

You can lend money to the company for the deposit from your personal assets.

Mortgage Lenders prefer companies that will only own and rent property. They dislike trading companies doing other activities.

Is it harder to get a Buy to Let in a Limited Company?

It's not generally more difficult in term of criteria than purchasing in a personal name. In some instances (such as rental stress tests) it may be easier to buy in a Limited Company.

The number of mortgage products is restricted compared to the personal name, though it has been getting larger.

Trading Company or SPV Company?

Mortgage Lenders do not like to lend to Trading Companies. They see the other activities as a potential risk.

The preferred method is a Special Purpose Vehicle (SPV).

You can obtain BTL Mortgages in a Trading Company, but your mortgage product options are limited.

What is an SPV Limited Company?

A Special Purpose Vehicle (SPV) is a Limited Company incorporated at Companies House as a Buy to Let Holding Company.

The lender requests this Company’s activities be limited to undertake property rental activities only.

If the company, for example, sold Widgets as well; that would not be an SPV but a trading company.

Who owns the property?

The Company.

An LTD Company is a “separate legal entity” that obtained finance to purchase the property in its name.

You will have a personal guarantee to the bank, that does not mean you have personal ownership rights.

So the Company owns the Property, but you will hold the Company based on the % of shares.

Each shareholder will need to be named on the application, provide details and a personal guarantee.

You can be 100% shareholder.

Will the lender require a personal guarantee?

Yes - when buying property in an SPV Limited Company the directors and shareholders are often required to sign personal guarantees.

The personal guarantee requirement is mostly compulsory, except in exceptional cases where the Loan to Value (LTV) is very low. In such cases, a charge on the company as a whole may be taken - though this is a rare occurrence.

Asking a lender to take a risk by lending you the money, but requesting to not to give those same guarantees personally. As you imagine is not looked upon lightly.

A personal guarantee is a backstop - if the asset depreciates or missed payments. The lender has the equity (minimum 15% Deposit) as a safety buffer first. Therefore offering a personal guarantee may be seen as a medium risk. With the personal guarantee released on full repayment to the lender (such as selling the property).

In recent times the buy-to-let mortgage market has seen a significant switch in how landlords buy properties. An increased amount of corporisation.

Landlords are now, in more significant numbers, forming Limited Company's to buy, hold and rent out properties. The companies are typically new, perhaps a day old. Have no income or assets!

So how can the company get a mortgage? Mortgage lenders ask for a Personal Guarantee.

A personal guarantee gets around the "limited liability" an LTD Company typically offers and puts you the shareholder/director on the line for the debt.

Allowing a mortgage lender to assess your circumstances, your income and your assets. It has given them reassurance that in the event of a default they can pursue any unpaid amounts from you.

Most mainstream mortgage lenders require a personal guarantee. Though not all!

A personal guarantee, as above, aim to limit the lender's liability and risk. Obtaining a buy-to-let mortgage without a personal guarantee is possible If purchased at Low Loan to Value (LTV).

As a general rule, the few lenders that offer this, are looking at 60-65% Loan to Value (LTV).

With equity of at least 30-35% in the property, the lender can feel secure that they will get their funds back in the event of a default.

The reason for such substantial equity required it to allow them to add any missed mortgage payments, fines and allow for housing price fluctuations or damage to the asset.

With the rarity of lenders offering buy to let mortgages without a personal guarantee. There is a premium to pay, at mortgage rates today an LTD Co SPV at 65% can enjoy mortgages at 2.49% without a personal guarantee 2.94%.

Limited Company Buy to Let FAQ

Landlords nationwide are discussing the Advantages and Disadvantages of Limited Company Buy-to-Let. We will look at some of the questions raised.

Can I buy a property in a Limited Company?

Yes. Lenders offer products for purchasing properties in companies.

Are Ltd company buy to let mortgages hard to get?

No. Mortgage lenders have products that can buy properties in a Limited Company.

There are fewer mortgage lenders but the criteria and products are wide-ranging.

How do I set up a Limited Company?

You can ask your Buy to Let Mortgage Broker to incorporate a company on your behalf.

You can incorporate £15+VAT online or ask your accountant.

The company can not undertake any other activities, just the buying and renting of property.

As such you are required to use one of the following SIC codes:

- 68100 - Buying and selling of own real estate

- 68209 - Other letting and operating of own or leased real estate

When you incorporate you don't often provide a SIC code, if the lender requires it you can do so by filing on annual returns.

Ask your mortgage broker for advice.

A new company has no history or income!

That is right! Mortgage Lenders prefer a none trading companies.

They want a Special Purpose Vehicle (SPV) a company that does nothing other than renting out property.

If its a new company with no history - then that is perfect. If you already have a company renting property (only) then that is fine too.

If you already have a trading company, perhaps you are an IT Consultant. It will have history, liabilities and other activities.

That is risky to mortgage lenders.

How old does the limited company have to be?

Mortgage Lenders will accept limited companies as soon as they have been set up. We allow day 1 SPVs.

But... Id prefer my Trading Company to buy a property?

You can! but your options will be limited.

Other options may include:

- Trading Company, incorporating a SPV it owns.

- Trading Company, providing loan to your SPV.

You should talk to your mortgage broker to discuss such options. The route may be what the available lender prefers.

How is affordability assessed?

Lenders assess affordability on Limited Company Buy to Let mortgages on two things:

- You Personally! (and any other shareholders/directors)

- The Property.

Mortgage lenders affordability test is no different to buying in a personal name.

Lenders will want to ensure you have some income to cover void periods and others have minimum income requirements.

You will be credit checked as usual.

Lenders will stress test the rental income. ( How is Buy-to-let Affordability assessed? )

Does a limited Company mean Limited Liability?

On application to a mortgage lender, you will wave your "limited liability".

Every shareholder and director of the company will be required to provide a Personal Guarantee.

That means - if your rental company fails to pay the mortgage. They can then pursue you.

Will they take a charge on my home?

No. Providing a personal guarantee does not mean a lender will take a charge on your home.

If a lender has to repossess a property in a limited company and is still owed money. The person offering the Personal Guarantee will be liable for that money.

This is the same if you buy in your own name.

How does the deposit work?

You will need a deposit! but how do you get it into the company.

Many mortgage lenders insist you GIFT the deposit funds to the company from your own savings.

Accountants prefer a different way.

Some mortgage lenders allow you to LOAN the deposit funds to the company from your own savings.

This will make your accountant happy, repaying the loan back to yourself from the company is tax free.

Ask your accountant for advice on tax proposition. Your mortgage broker will confirm which lenders allow which route.

Will I need a bigger deposit?

No. You can get Limited Company Buy to Let at 85% Loan to Value.

You will find better mortgage rates and more options at 75% LTV or lower.

Costs: Personal v Company

The costs for a Limited Company Buy to Let tend to be higher than in a personal name.

A mortgage lenders Arrangement Fees and Mortgage Rates are typically higher for a Limited Company - from 1% to 1.5%.

In recent months this has started evening out. It was announced Aldermore was to join Paragon Mortgages in charging same interest rates.

Your Conveyancing Solicitor may charge higher fees. This is due to the increased legal complications. ( Why is Conveyancing more expensive? )

You will have Company Requirements such as filing Annual Returns and Filing Accounts. There is a small fee at Companies House. The greater costs are for professional accountants to complete these for you.

Whose Money is it?

A limited company has its own legal personality, which is separate to the individuals who participate in it.

You should establish a separate bank account for the separate legal entity.

You can not spend the rent the company earns on things other than business activities.

If you do so it will be a Wage or Benefit and this will effect your tax position.

It is the companies money. It is only yours when it is transferred to you and taxed accordingly.

How does the Tax Work?

You need to talk to your accountant about Tax Planning in a Limited Company.

After legislative changes on Mortgage Interest Relief - Limited Companies became a popular option.

This arises as companies are able to "retain profits".

This allows you to plan with your accountant what the company will pay you. You can plan what your personal tax position will be.

Do I need a Separate Bank Account?

Yes. Your own bank should be happy to provide you with a Company Bank Account.

It is typically not a mortgage condition but can affect your tax position.

It will make it easier to separate the companies funds from your funds. Especially when filing accounts for simplicity.

How do I sell a property?

You can sell a property as you would do normally.

The profits will belong to the Limited Company and not you personally.

You can re-invest or withdraw monies and be taxed accordingly.

A different route is, you could sell the whole company. The buyer instead of buying the property, buys the company that owns the property.

You will need advice. Put simply you sell then the shares and on the same day the buyer re-mortgages.

The refinance will remove your personal liability on the existing mortgages.

What if I re-mortgage or get a 2nd Charge?

Any further equity you release will belong to the Limited Company and not you personally.

You can re-invest or withdraw monies and be taxed accordingly.

How many people can be part of the company?

You are typically looking at a maximum of Four Shareholders / Directors. Which opens up opportunities for Joint Ventures.

You can have more parties but lending options reduce.

Can I get Bridging Finance in a Limited Company?

Yes. Limited companies can get bridging finance.

This is typically used if the property is uninhabitable and requires work to make it mortgageable.

Or if you require to purchase the property fast, such as in an auction.

Can I buy a HMO in a Limited Company?

Yes. Limited Companies can get mortgages for buying a House of Multiple Occupation (HMO).

At the time of writing Limited Companies can buy HMO properties at 85% LTV.

Can I transfer property from personal to Limited Company?

Yes and No.

You can not transfer them as a company is a separate legal entity.

You can re-mortgage the properties into a Limited Company.

Some lenders require you to have the deposit in cash. Others allow a paperwork transaction - using the same equity.

This can be known as "gifted equity" or in rare cases "loaned equity".

Talk to your Mortgage Broker about SDLT and Capital Gains

-

Buy-to-Let Mortgage

>

Dive into property investment with our Buy-to-Let Mortgage, tailored for both seasoned investors and first-timers seeking to build a profitable portfolio.

-

Buy-to-Let Remortgage

>

Maximize your investment with Buy-to-Let Remortgage, ensuring optimal returns by refinancing your property portfolio with competitive rates.

-

Buy-to-Let Rate Switch

>

Enhance your property investment strategy with a Buy-to-Let Rate Switch, ensuring you stay competitive in the market with a smart financial move.

-

Buy-to-Let Company Mortgage

>

Optimize your property portfolio's potential with a Buy-to-Let Mortgage in your SPV Company Name, combining strategic investments with simplified financial structures.

-

Portfolio Mortgages

>

Grow and diversify your property portfolio with our Portfolio BTL Mortgages, offering tailored solutions for seasoned investors aiming for prosperity.

-

Holiday Let Mortgage

>

Transform your vacation home investment dreams into reality with a Holiday Let Mortgage,

-

HMO Mortgage

>

Unlock the potential of shared living spaces with our HMO Mortgage, tailored to support your investment in Houses in Multiple Occupation.

-

HMO Company Mortgage

>

Elevate your HMO investment strategy with our HMO Mortgage in your SPV Company Name, combining strategic planning with streamlined financial structures.

-

HMO Remortgage

>

Revitalize and optimize your HMO investment with a strategic HMO Remortgage, ensuring your shared living spaces remain lucrative in the market.

Get in touch

We are your online mortgage broker, offering you the convenience of applying for a mortgage online. However, we understand that sometimes you may prefer to speak with a human - phone, email or in person.

- Phone number

- 01133 205 902

- [email protected]

- Postal address

-

31 Bradford Chamber Business Park,

New Lane, Bradford, BD4 8BX

Looking for career in Mortgage Advice? View job openings.

We are authorised and regulated by the Financial Conduct Authority (No. 919921). The FCA does not regulate most Buy to Let mortgages.

Think carefully before securing other debts against your home. Your home may be repossessed if you do not keep up repayments on your mortgage.

Cyborg Finance Limited is registered in England and Wales (No. 12131863) at Bradford Chamber, New Lane, Bradford, BD4 8BX